- February 4, 2026

-

-

Loading

Loading

In Florida, 2022 might go down as the year of the credit union. An explosion of organic and inorganic growth, along with banking industry consolidation, has seen credit unions flexing their muscles and spreading their wings like never before.

According to the latest data from the Credit Union National Association, the average total assets per credit union grew from $360.1 million in 2015 to $776.5 million in 2021, up 115.63%. Membership per credit union rose during that time from 5,215 to 6,645, up 27.42%.

Meanwhile, some 93.8% of Florida credit unions posted an increase in assets in 2021, down slightly from 98.4% in 2020 but up significantly from 82% in 2015.

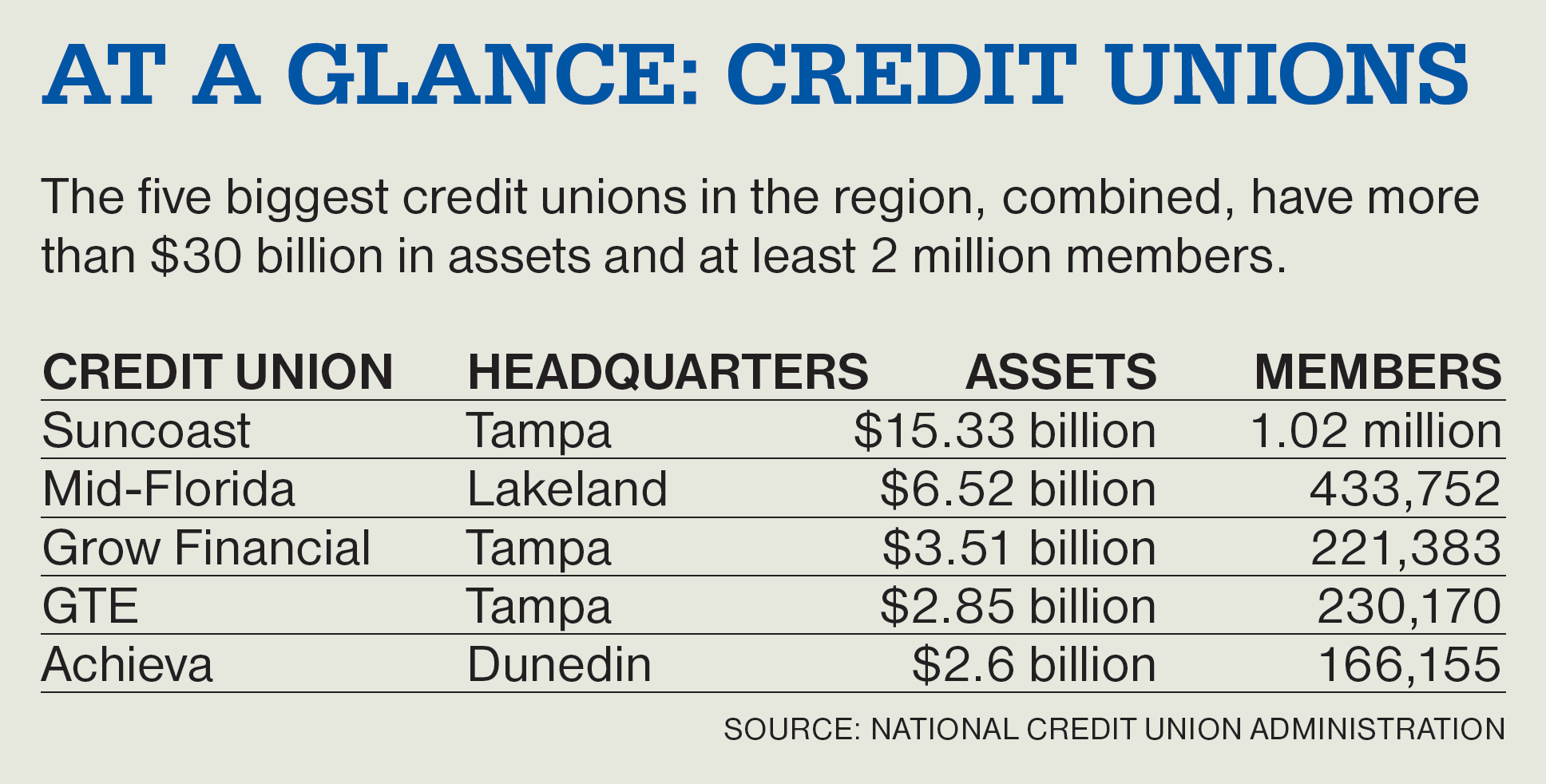

At the top of the heap is Tampa-based Suncoast Credit Union, with $15.33 billion in total assets through Dec. 31. “The bigger we get, the greater economies of scale we gain,” Suncoast Credit Union Chief Growth Officer Darlene Johnson says, “and that gives us the opportunity to be more efficient; it gives us the opportunity to have better vendor negotiations, which puts more more money in our arsenal, which gives us the ability to give more money back to our members.”

Including Suncoast, four of the top 10 biggest credit unions in the state — MidFlorida Credit Union in Lakeland and Grow Financial Credit Union and GTE Credit Union, both in Tampa — are based in the Tampa Bay region, while Dunedin-based Achieva Credit Union is No. 11 on the list. And then there’s the trend of newly emboldened credit unions, both in Florida and out of state, buying community banks.

Not everyone is thrilled about the rise of jumbo-sized credit unions. The Florida Bankers Association has for years lobbied the government to force credit unions that have total assets upward of $500 million to pay federal and state income taxes.

“We have a $30 trillion national debt,” FBA President and CEO Alex Sanchez says in an interview with the Business Observer. “Why are we giving tax subsidies to multibillion-dollar financial institutions? Why does a family of four pay more in state and federal taxes than a multibillion-dollar credit union?”

Given the pandemic-driven flood of people moving to all corners of Florida, a credit union would have to be totally inept not to have grown organically in recent years.

“We’re fortunate to live in the state of Florida,” MidFlorida Credit Union President and CEO Steve Moseley says. “We’ve got significant net growth here. In some of our smaller markets, like Highlands County, a lot of national banks have pulled out. We are investing and staying in the smaller markets, so we’ve naturally picked up a lot of members. When banks close branches people have to get banking (services) somewhere.”

Moseley says MidFlorida has set a goal of adding 66,000 new members this year, and is ahead of the pace it will need to reach that milestone by about 4,000 accounts. Organic growth, he adds, is coming from “everywhere,” citing disruption and consolidation among banks as a major factor, along with MidFlorida’s indirect lending program in which car dealers write loans that funnel car buyers into the MidFlorida ecosystem.

“And we’re continuing to add branches,” Moseley adds, “and that creates new members for us, as well.”

Achieva Credit Union COO Jennifer Galley, meanwhile, has sussed out some intriguing trends from her institution’s recent surge of organic growth. While migrants to Florida are “a huge part” of Achieva’s cohort of new members, “we are seeing more and more snowbirds come down and stay longer, or not go home at all. And we’ve had a Hispanic (marketing) initiative for several years now. We see that population really starting to grow within our ranks of members.”

Galley says Achieva’s membership base has grown 11% year-over-year, and, like MidFlorida, much of that increase has been derived from indirect lending, such as auto loans. “That’s adding a lot of new members,” Galley says. “We’re trying to put more resources into converting those people who don’t really understand what a credit union is, or what membership means to them, into being more engaged, multi-product members.”

With more out-of-state banking players entering the Florida market, credit unions, to maintain and grow market share, have also picked up the pace of acquisitions. In doing so, some credit unions are targeting the state’s dwindling supply of community banks.

A straight-up credit union bank acquisition was virtually unheard of as recently as 2015. But that year, Achieva lit the fuse of the trend when it bought, for $23.2 million, Punta Gorda-based Calusa Bank. In 2018, Achieva bought Fort Myers-based Preferred Community Bank, which, at the time, had $116 million in assets, for an undisclosed sum.

Both moves significantly expanded Achieva’s footprint. Yet the deals came with some unique integration challenges, Galley says.

“When you’re acquiring a bank, both the employees and the customers are likely to not understand what a credit union is, how they operate and how they’re similar to and also very different (from banks). For some members, they actually have a lot of fear around not understanding what a credit union is, or even just the word ‘union’ can be intimidating. They associate it with labor unions and all kinds of other things.”

Converting bank customers to credit union members can also be tricky because they are required to proactively opt in. Sometimes, Galley says, some education, guidance and most of all, patience, is required.

“It’s important that every single one of the customers understands what that means and is comfortable completing that opt-in process,” Galley says. “What we found is for the handful of people who don’t understand, or are uncomfortable with the idea, we appeal to them to give us a try. And if, after they’ve facilitated some of their banking needs with us, they’re not happy, we can revisit the conversation, and usually by then we’ve won them over. But there are no strings tied to giving us a shot.”

MidFlorida Credit Union is another hunter of banks. In 2019 it acquired Ocala Community Bank & Trust of Florida, a $730 million-asset bank. It also bought the assets of First American Bank of Iowa, with holdings that include a $240 million commercial and residential mortgage portfolio, mostly in the Naples and Cape Coral markets.

Moseley says MidFlorida targeted Ocala Community Bank & Trust out of a desire to expand its services, not just its geographical footprint. The bank had a strong treasury services department, and adding that to MidFlorida’s offerings has been a source of “good, solid growth,” he says.

As credit unions have gotten bigger and bigger, however, they’ve run afoul of bankers and advocates for the industry, such as Sanchez, who’s quick to point out the vast majority of credit unions — 80% to 85%, in his estimation — don’t fall into the “too big” category. Those aren’t the ones his organization is concerned about.

“The milkman’s union used to be for the milkman,” he says. “But Navy Federal Credit Union is over $150 billion in size. They’re bigger than our regional banks. They say, ‘We’re not-for-profit.’ No, no, no — you are a bank, and you’re making a lot of money. And you should support the needs of our country and our society and our state.”

Credit union executives, on the other hand, say such characterizations miss the point — namely, there are fundamental differences that separate banks from credit unions and, as Galley points out, those differences are often not well known.

“Credit unions have a voluntary board of directors,” she says, “and their sole focus and motivation is helping people be financially independent. Anything that threatens that design, I think, is not positioning us to help empower our members.”

Sanchez agrees there’s a clear need for credit unions. But he disagrees with the way the industry uses small, “mom and pop” credit unions to represent itself in Congress.

“I am not talking about them,” Sanchez, referring to small credit unions. “Leave them alone. Put them aside.”

Sanchez is talking about Jacksonville-based Vystar Credit Union, which has more than $12.3 billion in total assets. Last year Vystar announced an agreement to acquire Heritage Southeast Bank, a Jonesboro, Georgia, bank with $1.5 billion in assets. Although the parties terminated that agreement June 15, if it had gone through, Vystar would have bought a bank that, if based on the west coast of Florida, would easily be one of the biggest in the region. Sanchez is also critical of Dearborn, Michigan-based DFCU Financial, which in early May agreed to a deal that will see it acquire Tampa’s First Citrus Bank.

“They’ve gone way beyond their mission,” he says, “and quite frankly, our country cannot afford this type of corporate welfare anymore.”

This article has been updated to reflect that the agreement for Vystar to acquire Heritage Southeast Bank was terminated June 15.